(804) 353-4500tswinfo@tswinvest.com

You are leaving TSW

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

There has been a general belief in the industry that as one migrates further up the market capitalization ladder, market efficiency is greater, therefore creating a more difficult backdrop to generate alpha. In our opinion, this historically may have been true on the margin compared to mid- and small- caps, but certainly not to a level that would be prohibitive for active management to outperform, particularly within value. More importantly, the microstructure of the market has changed dramatically over the last 10-20 years (i.e., impact from passive which is purely a price momentum driven strategy, spike in retail investor involvement, short-term orientation from many institutional investors, etc.) that has created inefficiencies across the market cap spectrum from small to large cap equities. At TSW, we believe markets are inefficient in shorter time periods, but efficient over a longer time, creating ample investment opportunities. We believe this change in microstructure has significantly exacerbated short-term inefficiencies creating a greater case for active management across market capitalizations that we don’t see changing.

Within the Large Cap spectrum of investing, there is a material difference between the construct of the Russell 1000® Value Index and Russell 1000® Growth Index, which has had a large impact on the active versus passive debate. Specifically, the Russell 1000® Growth Index has historically been top heavy with the top 5 positions representing 37.4% of the Index on average over the past three years ending 6/30/2023 (reached north of 40% over the last two years), compared with 10.9% for the Russell 1000® Value Index. This top-heavy nature of the Growth index has arguably created much wider variability of relative returns for active large cap growth managers, predicated heavily on a manager’s underweight or overweight to Apple (13.4% of index as of 6/30/2023), Microsoft (11.7% of index as of 6/30/2023), and the rest of the mix. Furthermore, as of 6/30/2023, there were 844 stocks in the Russell 1000® Value Index, compared to 444 stocks in the Russell 1000® Growth Index, providing additional context for the more diversified and less concentrated nature of the Index on the value side. We highlight this point to illustrate the unique differences of the large cap universe on the value side that we believe sometimes get erroneously grouped into its growth counterpart. We ultimately believe the Large Cap Value universe contains an attractive and diverse opportunity set for active management that is not dictated heavily by behemoths in the Index.

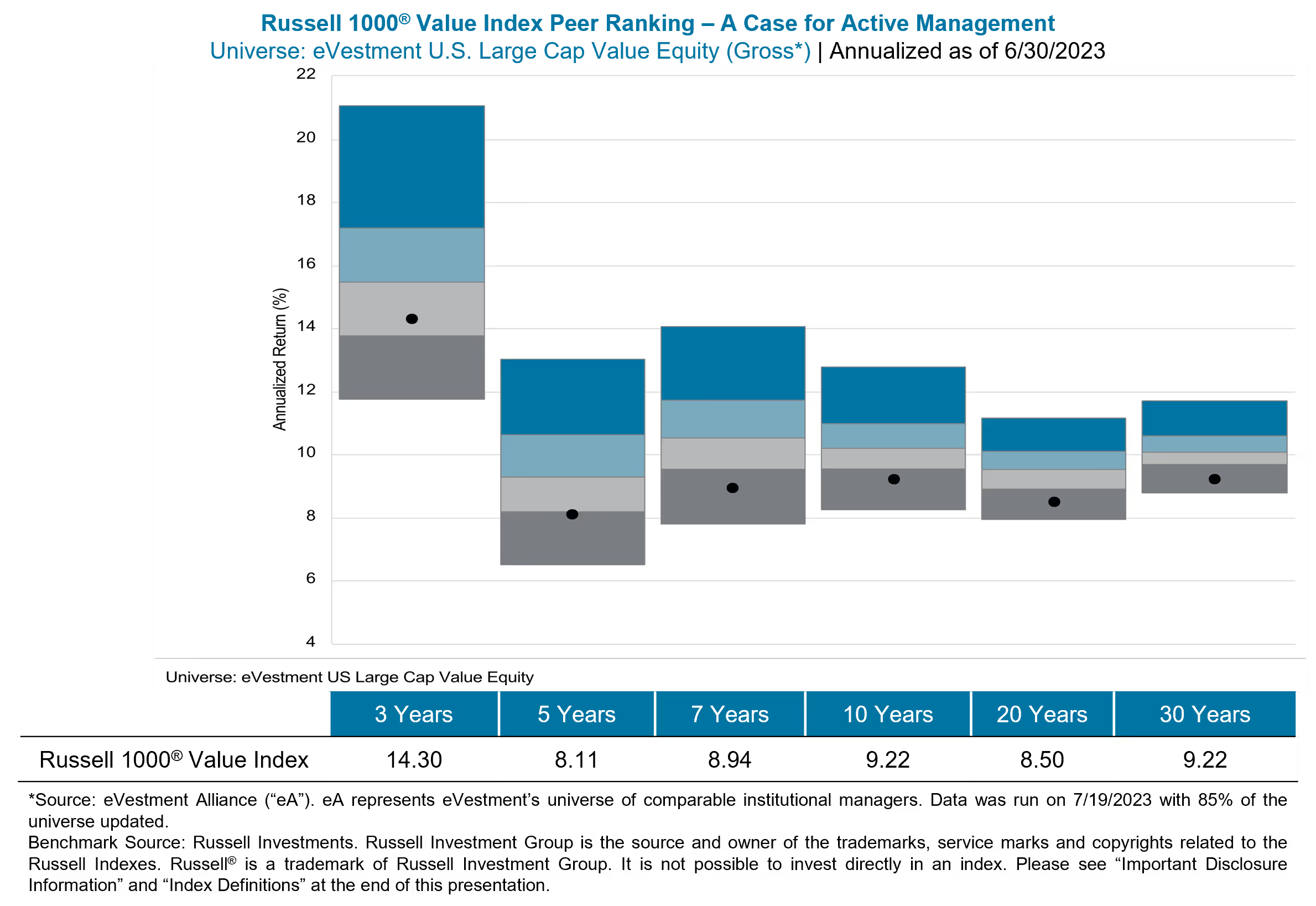

Active Large Cap Value in buy and hold approach: Contrary to popular belief, active large cap value managers have outperformed the Russell 1000® Value Index over the majority of trailing time periods. In fact, as highlighted below in chart format, over the last 3, 5, 7, 10, 20 and 30 years through 6/30/2023, the Russell 1000® Value Index has placed in or near the bottom quartile of eVestment’s Large Cap Value active management peer group. We believe the historical success of active large cap value managers, in conjunction with the changing market microstructure mentioned above, presents a very sound argument for an active allocation in Large Cap Value.

An All-Cap Alternative: Large Cap Value is inherently all-cap. As of 6/30/2023, the smallest stock in the Russell 1000® Value Index was sub-$1 billion in market capitalization while the largest was in excess of $1 trillion.

The TSW Mid Cap Value team assumed responsibility of TSW’s Large Cap Value strategy on 8/31/2015, tasked with transitioning the assets into a concentrated 30-40 stock portfolio while adhering to the same philosophy and process used for nearly 20-years in running our domestic Mid Cap Value strategy.

Consistent and Balanced Performance Expectations: TSW Large Cap tends to do well in most market environments when valuation and fundamentals are reflected in stock prices. This has coincided with relatively strong periods of return in both up and down markets, and style purity throughout time, all while delivering results with much less volatility than the Index and other Large Cap Value peers.

Consistent Value Characteristics: We consider ourselves Traditional Value in that we’ve been consistently priced at a discount to the Russell 1000® Value Index, as we are price sensitive in our bottom-up fundamental approach.

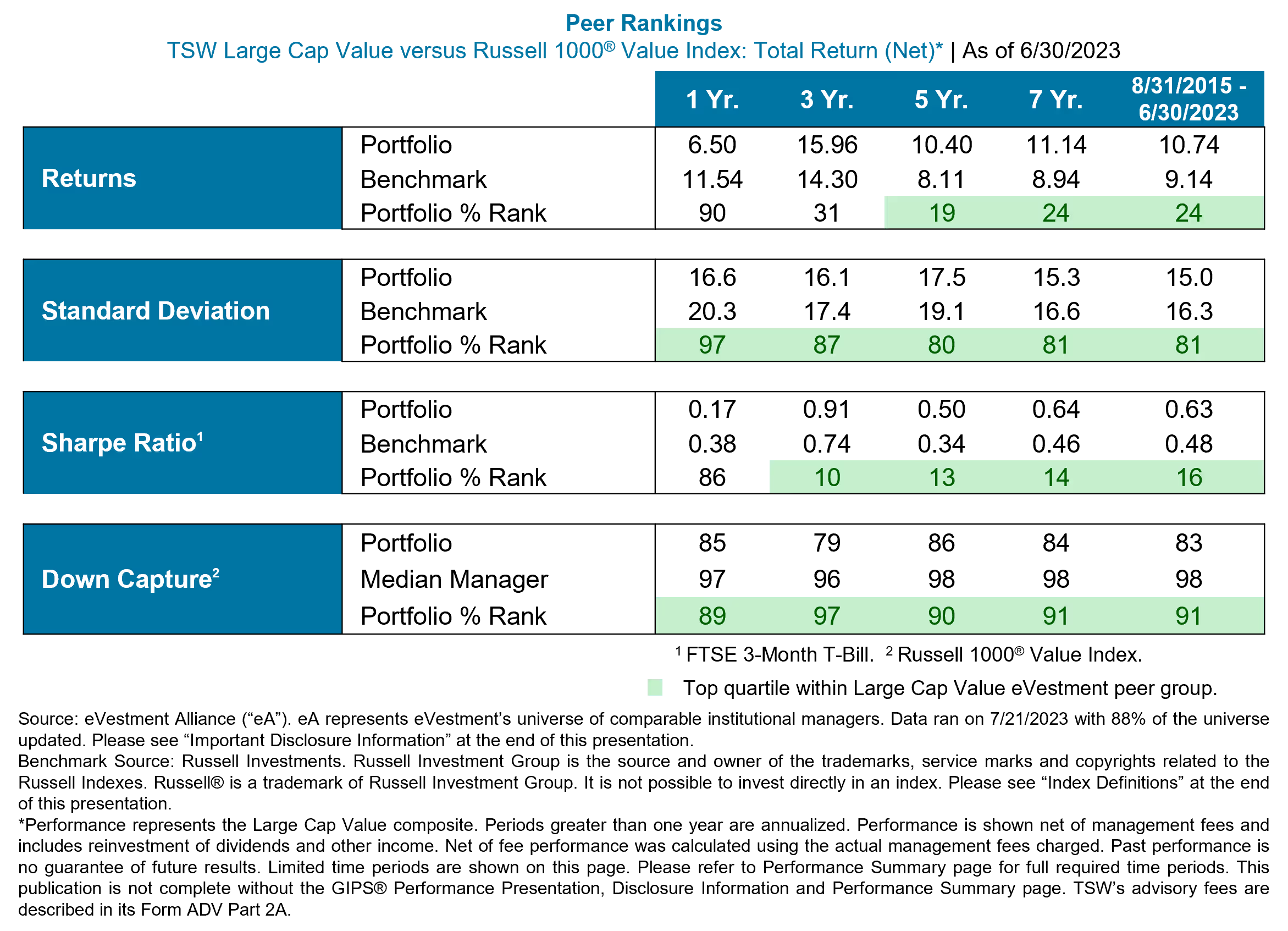

Ripe Opportunity for Value and TSW: While the TSW Large Cap Value composite has outperformed the Index, net of fees, across the 3-yr, 5-yr, 7-yr and since the current Portfolio Management team took over on 8/31/2015 (through recent quarter end), much of its existence with the current team coincides with prominent growth years ending 2020, and the more egregious irrational and anti-value period in 2023 thus far. This was accomplished despite our style purity and consistent discount to the value Index. We believe our ability to protect capital in most down-markets and persistent discount to the value Index remains an attractive posture given not only what we believe to be a more sustained multi-year rotation towards value, but one where uncertainty in the markets remains at heightened levels.

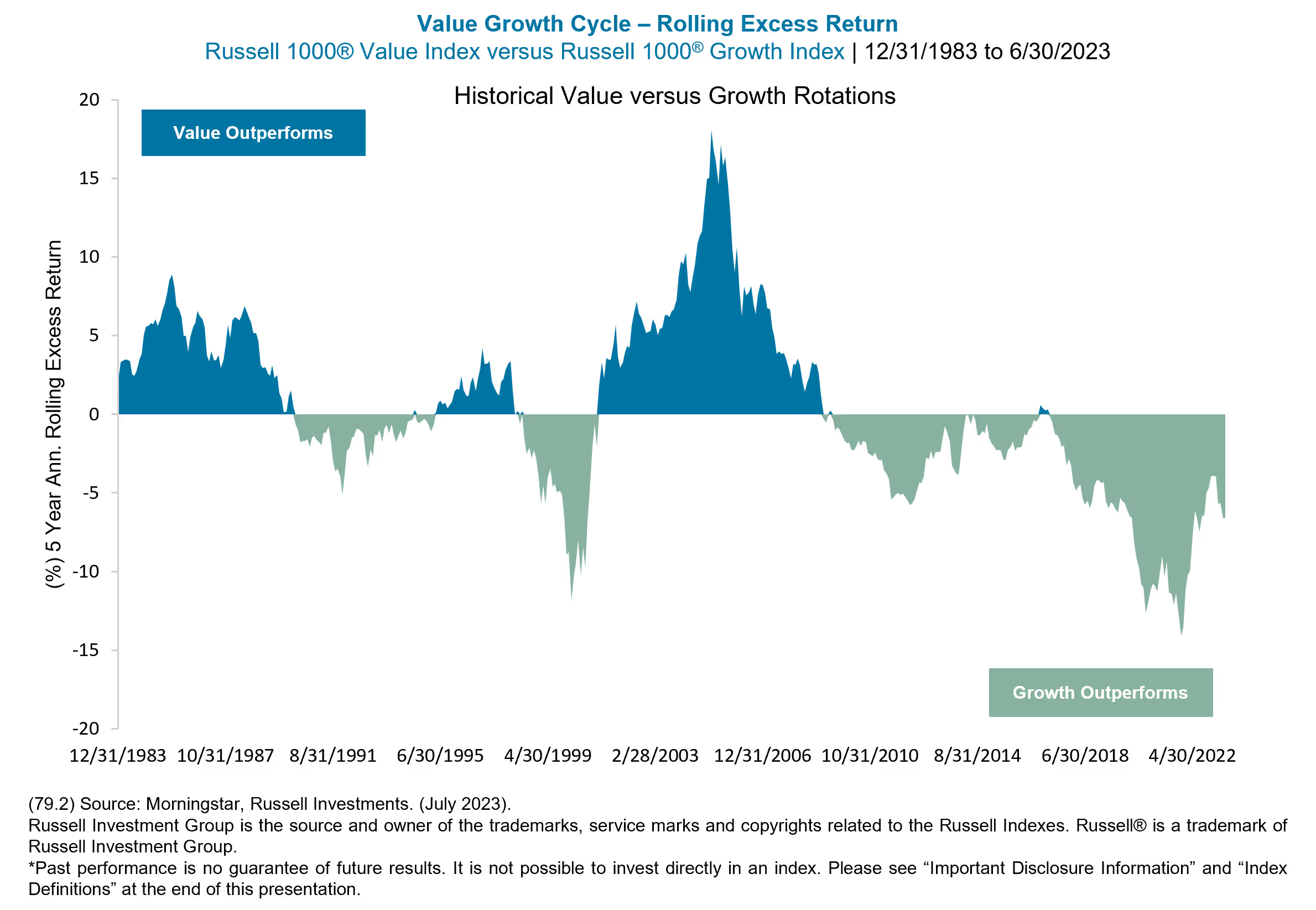

Following a 12-year growth cycle from 2009 through 2020 where the Russell 3000® Value Index underperformed its growth counterpart by more than 390% cumulatively, 2021 forward has generally been a ripe (albeit, volatile) time for value. That being said, much of the value run was concentrated in less than a year where value had a favorable period of performance from late 2021 through the first half of 2022. More recently, however, the market appetite in favor of a mere handful of mega cap growth technology stocks has brought what we had deemed to be early innings of a sustained value rotation (perhaps 2nd or 3rd inning prior to 2023) to arguably closer to the 1st inning.

We ultimately believe value’s current historic discount to growth provides an incredibly promising future and outlook. For historic context, the decade of the 1990s was phenomenal for growth investors as the dot.com craze heated up during the middle of the decade and was capped off by an incredible run over the years 1998, 1999, and very beginning of 2000. After the bubble burst in March of 2000, it took another seven years for growth to hit bottom relative to value.

We do not know what the future holds but believe the current state of the market looks awfully similar to what was witnessed after the dot.com bubble burst. As highlighted, we believe value is positioned for a sustained favorable rotation, but do note that any cycle shift is never a straight line, and this period will be no exception.

GIPS® Disclosures: Large Cap Value

IMPORTANT DISCLOSURE: This commentary is intended for informational purposes only and does not constitute a complete description of our investment services, analysis, or performance. This commentary is in no way a solicitation or an offer to sell securities or investment advisory services. The expressed views and opinions contained herein are for informational purposes only, are based on current market conditions, and are subject to change without notice. Although information, opinions, and statistics contained herein have been obtained from sources believed to be reliable and are accurate to the best of our knowledge, Thompson, Siegel & Walmsley LLC (“TSW”) cannot and does not guarantee the accuracy, validity, timeliness, or completeness of such information and statistics made available to you for any particular purpose. This commentary should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Past performance is not indicative of future results. No part of this commentary may be reproduced in any form, distributed, or referred to in any other publication, without express written permission of TSW.

EVESTMENT DISCLOSURE: eVestment Alliance, LLC and its affiliated entities (collectively, “eVestment”) collect information directly from investment management firms and other sources believed to be reliable, however, eVestment does not guarantee or warrant accuracy, timeliness, or completeness of the information provided and is not responsible for any errors or omissions. The eVestment Universe ranking is calculated by eVestment using investment performance returns and strategy descriptions self-reported by participating investment managers and are not verified or guaranteed by eVestment. eVestment defines each Universe and selects the participating managers for the Universe it determines have similar investment strategies.

Performance results may be provided with additional disclosures available on eVestment’s systems and other important considerations such as fees that may be applicable. Performance returns for periods greater than one year are annualized. Additional information regarding performance rankings is available upon request.

Not for general distribution and limited distribution may only be made pursuant to client's agreement terms. Copyright 2012-2023 eVestment Alliance, LLC. All Rights Reserved.

Performance represents the Large Cap Value composite. Periods greater than one year are annualized. Performance is shown gross of management fees and includes reinvestment of dividends and other income. Gross returns will be reduced by investment advisory fees and other expenses that are incurred in the management of the account. Past performance is no guarantee of future results. Limited time periods are shown on this page. Please refer to Performance Summary for full required time periods. This publication is not complete without the GIPS® Performance Presentation, Disclosure Information and Performance Summary . TSW’s advisory fees are described in its Form ADV Part 2A. It is not possible to invest directly in an index. Please see “Important Disclosure Information” for detailed performance disclosure and the index description.

Inception date is 8/31/2015. As of 9/1/2015, the TSW Large Cap Value strategy is managed by current portfolio management team.

GENERAL ECONOMIC & MARKET COMMENTARY DISCLOSURE: Comments and general market related projections are based on information available at the time of writing and believed to be accurate; are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm and may not be relied upon for future investing. Certain information contained in this material represents or is based upon forward-looking statements, which can be identified by the use of terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of an Account may differ materially from those reflected or contemplated in such forward-looking statements. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results.

BENCHMARK SOURCE: Russell Investments. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

INDEX DEFINITIONS:

- Russell 1000® Value Index: The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years).

- The Russell 1000® Growth Index: The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years).

- Russell 3000® Value Index: The Russell 3000® Value Index measures the performance of the broad value segment of the US equity value universe. It includes those Russell 3000 companies with relatively lower price-to-book rations, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years).

EQUITY SECURITIES RISK: Equity securities generally have greater risk of loss than debt securities. Stock markets are volatile, and the value of equity securities may go up or down, sometimes rapidly and unpredictably. The value of equity securities fluctuates based on real or perceived changes in a company’s financial condition, factors affecting a particular industry or industries, and overall market, economic and political conditions. If the market prices of the equity securities owned by the strategy fall, the value of your investment in the strategy will decline. Your portfolio may lose its entire investment in the equity securities of an issuer. A change in financial condition or other event affecting a single issuer may adversely impact securities markets as a whole.

PRINCIPAL RISK: Risk is inherent in all investing. Many factors and risks affect performance. The value of your investment, as well as the amount of return you receive on your investment, may fluctuate significantly day to day and over time. You may lose part or all of your investment in your portfolio or your investment may not perform as well as other similar investments. An investment in the strategy is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money if you invest in this strategy.

VALUE INVESTING RISK: The prices of securities TSW believes are undervalued may not appreciate as anticipated or may go down. The value approach to investing involves the risk that stocks may remain undervalued, undervaluation may become more severe, or perceived undervaluation may actually represent intrinsic value. Value stocks as a group may be out of favor and underperform the overall equity market for a long period of time, for example, while the market favors “growth” stocks.

© 2023 Thompson, Siegel & Walmsley LLC (“TSW”). TSW is an investment adviser registered with the SEC. Registration does not imply a certain level of skill or training. All information contained herein is believed to be correct but accuracy cannot be guaranteed. TSW and its employees do not provide tax or legal advice. Past performance is not indicative of future results; past performance does not guarantee future results, and other calculation methods may produce different results. There is the possibility of loss of principal value. Certain GIPS® disclosures are provided on TSW’s website at www.tswinvest.com, others are available upon request. TSW is a trademark in the United States Patent and Trademark Office.

Subscribe to receive the latest news and updates

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.